For Daily Job Alert For Daily Job Alert |

Join Our Whats App Channel |

| For Free Study Material |

Join Our Telegram Channel |

Simple and Compound Interest Tricks – 1

(1) The basic concept of CI and SI

Let’s say you have Rs. 30000 and you keep this money in three different banks for 2 years(Rs. 10000 each). The three banks have different policy :

a) Bank A keeps your money at simple interest and offers you 5% interest

b) Bank B keeps your money at compound interest and offers you 5% interest. The interest is compounded annually.

Bank C keeps your money at compound interest and offers you 5% interest. The interest is compounded half-yearly.

After 2 years, which bank will give you most interest?

Let us calculate

Case (A)

Simple interest is calculated simply as (P*R*T)/100

Here P= 10000, r = 5% and T = 2 years

T = 2 years. Let’s divide this period in two equal intervals of 1 year each

Hence SI received for the period 0 to 1 = 10000*5*1/100 = Rs. 500

SI received for the period 1 to 2 = 10000*5*1/100 = Rs. 500

So after 2 years, you will get Rs. 10000 + 500 + 500 = Rs. 11000

Note : Simple Interest is proportional. The interest received is same each year. So in the above example where SI was Rs. 500 for 1 years, that will mean the SI for 3 years is Rs. 1500, the SI for 5 years is Rs. 2500 and so on.

Case (B)

Compounded annually means whatever interest you will earn on first year, that interest will be added to the principal to calculate the interest for 2nd year. Let us see how

We know the CI formula is, Amount = P(1 + r/100)^t (where Amount = P + CI)

CI received for the period 0 to 1 = Amount – Principal = 10000(1 + 5/100)^1 – 10000= Rs. 500

Now the amount received after 1 year will act as the Principal for calculating the Amount for next year

For calculating the amount for second year, you won’t take P as 10000, but as Rs. 10500. So unlike SI where the interest was same each year, in CI the interest increases every year (because the principal increases every year)

CI received for the period 1 to 2 = Amount – Principal = 10500(1 + 5/100)^1 – 10500 = Rs. 525

Total interest received after two years = Rs. 500 + Rs. 525 = Rs. 1025

Total amount received after two years = Rs. 11025

Note : In Case (b), to calculate the amount received after 2 years, I had divided the calculation into 2 intervals. It was done just for the sake of explanation. You can calculate the amount received after 2 years directly by 10000(1 + 5/100)^2

Case (C)

Just like case (b), where Principal was getting updated every year, in case (c) we will update the Principal every 6 months (half-year)

Since I have given the explanation in case (b), so in this case I will directly apply the formula

Amount received after 2 years = 10000(1 + 2.5/100)^4 = Rs. 11038 approx.

So sum it up

Case A – amount received after two years= Rs. 11000

Case B – amount received after two years= Rs. 11025

Case C – amount received after two years= Rs. 11038

Case C is giving the maximum return and rightly so because in Case (C) principal is increasing every 6 months.

Important formulas for Compund Interest –

(2) A sum of money becomes x times in T years. In how many years will it become y times?

The approach to solve such questions is different for SI and CI

For SI : Formula = [(y – 1)/(x – 1)] * T

Q. 1) A sum of money becomes three times in 5 years. In how many years will the same sum become 6 times at the same rate of simple interest?

Solution : [(6 – 1)/(3 – 1)] * 5 = 5/2 * 5 = 12.5 years

Answer : 12.5 years

For CI : Formula = (logy/logx) * T

Now dont worry, I wont be asking you to study logarithms 🙂

But just remember one property of logs and that is enough to solve the questions

log(x y) = y.log(x)

Hence log(8) = log(23) = 3.log(2)

Q. 2) A sum of money kept at compound interest becomes three times in 3 years. In how many years will it be 9 times itself?

Solution : (log9/log3) * 3 … (1)

log9 = log(32) = 2.log(3)

Put this value in (1)

= 2.log(3)/log(3) * 3

= 2 * 3 = 6 years

Answer : 6 years

(3) Interest for a number of days

Here P = 306.25

R = 15/4 %

T = Number of days/365

Number of days = Count the days from March 3rd to July 27th but omit the first day, i.e., 3rd March

= 28 days(March) + 30 days(April) + 31 days(May) + 30 days(June) + 27 days(July)

= 146 days

We know SI = (P * r * t)/100

Answer : Rs. 4.59

(4) Annual Instalments

This is the most dreaded topic of CI-SI. Before giving you the direct formula, I would like to tell you what actually is the concept of annual instalments(if you only want the formula and not the explanation, you can skip this part. But I would like you to read it)

Suppose you want to purchase an iPhone and its price is Rs. 100000 but you dont have Rs. 1 lakh as of now. What would you do? You have two options – either you can sell your kidney (which most the iphone buyers do :D), or you can go for instalments. But if you want to buy the iPhone through this instalment route, the seller will incur a loss. How? Had you paid Rs. 1 lakh in one go, the seller would have kept that money in his savings account and earned some interest on it. But you will pay this Rs. 1 lakh in instalments and that means the seller will get his Rs. 1 lakh after several years. So the seller is incurring a loss. The seller will compensate for this loss and will charge interest from you.

x(1 + r/100)^3 + x(1 + r/100)^2 + x(1 + r/100)^1 + x … (1)

Now (1) should be equal to (2) because only then the two routes (instalment route and direct payment route) will give the same return and seller would have no problem in giving you the iPhone in instalments.

[Remember the above equation for solving questions of compound interest]

P + P*r*4/100 = (x + x*r*3/100) + (x + x*r*2/100) + (x + x*r*1/100) + x

[Remember the above equation for solving questions of simple interest]

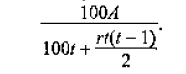

Although for Simple Interest, we have a direct formula-

The annual instalment value is given by-

Now coming to the questions. There are two types of questions and they are bit confusing. In one type, the Amount is given and in another type, Principal is given

Type 1(Amount is given):

Q. 4) What annual installment will discharge a debt of Rs.6450 due in 4 years at 5% simple interest?

When the language the question is like “what annual payment will discharge a debt of …”, it means the Amount is given in the question.

In this question, the Amount(A) is given, i.e., Rs. 6450. So we can apply the formula directly

Here A = 6450, r = 5%, t = 4 years

Solution : 100*6450/[100*4 + 5*4*3/4]

Answer : 1500

Type 2 (Principal is given) :

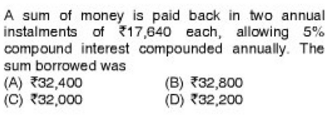

Q. 5) A sum of Rs. 6450 is borrowed at 5% simple interest and is paid back in 4 equal annual installments. What is amount of each installment?

But our formula requires Amount(A)

So we will calculate Amount from this Principal

A = P + SI = 6450 + 6450*5*4/100 = Rs. 7740

A = 7740, r = 5%, t = 4

Annual instalment = 100*7740/(100*4 + 5*4*3/2)

“Sum borrowed” means Principal.

This question is of Compound Interest and hence we cant apply the direct formula. We will solve this question with the help of the equation we derived earlier.

Answer : (B)

Q. 7) What annual instalment will discharge a loan of Rs. 66000, due in 3 years at 10% Compound Interest?

Solution : Here again the question is of “Compound Interest” and hence we will solve it by equation :

Let each annual instalment be of Rs. x. Note that in this question, amount is given

Amount = x(1 + 10/100)^2 + x(1 + 10/100)^1 + x

66000 = x (1.21 + 1.1 + 1)

So x = Rs. 19939.58

Q. 8) What annual instalment will discharge a loan of Rs. 66000, due in 3 years at 10% Simple Interest?

I have just converted Q.7 into Simple Interest

Now we can either solve it by direct formula, or by equation

By Equation method :

66000 = (x + x*10*2/100) + (x + x*10*1/100) + x

66000 = x(3 + 0.2 + 0.1)

x = Rs. 20000

By Direct formula method :

A = 66000, t = 3, r = 10%

x = 100A/[100t + t(t-1)r/2]

x = 100*66000/[100*3 + 3*2*10/2]

x = 6600000/(300 + 30)

x = Rs. 20000